The holiday season is upon us once again. There are a lot of things we associate with this time of year, but one of the most common has to be exchanging gifts with those we love. I can remember, as a child, writing out my wish list each year and the excitement I’d have wondering which gifts I might actually receive. Recalling those days I thought I would once again prepare a wish list, but with a little twist. Below you will find my holiday wish list to Congress and the IRS for changes I’d like to see made to the tax code.

Hurricane Sandy, also known as "Super-Storm Sandy," did considerable damage in the Northeast part of the United States. As a result, the IRS issued several news releases describing the postponement of certain tax-related deadlines for victims affected by Hurricane Sandy. These postponements also apply to IRA and other retirement plan deadlines. The relief applies to many counties in New Jersey, New York, and Connecticut.

The unified gift and estate tax exemption is scheduled to drop from $5,120,000 to $1,000,000 as of January 1, 2013. This has prompted IRA account owners, and some advisors, to consider gifting retirement assets to children and grandchildren. For Roth IRA owners this would seem to be an especially attractive strategy. Who wouldn’t want to move an income-tax-free asset that has no step up in basis out of their estate to their beneficiaries?

Last week, Hurricane Sandy - a.k.a. Frankenstorm - pounded the eastern part of the United States. In the days since, thousands have been displaced from their homes, more are still without power and millions have been financially impacted by the storm that, by some estimates, could top $50 billion in damages. Unfortunately, many of those who’ve been affected could be about to make - or may have already made – a bad situation worse by making costly financial and tax mistakes or top of the losses suffered as a result of Hurricane Sandy.

Mr. President,

As part of the campaign process for your bid to seek a second term in the White House, you recently released a copy of your 2011 tax return. Purely to satisfy my own curiosity, I decided to review the return, as well as the tax return of your challenger, Governor Romney.

The Slott Report's Election Week 2012 coverage is coming to a close, just as a "mega" storm has its eyes set on the Northeast and Election Days is just 11 days away. We hope you refer back to our coverage all week to determine what IRA, tax and retirement planning issues you should read up on before the Election and watch out for no matter who comes out victorious.

The tax code allows a taxpayer to plan his financial affairs so as to pay the least amount of tax that is legally owed. This allows individuals to take advantage of favorable tax provisions. But the lack of bipartisanship engaged in by Congress is making it harder and harder for individual taxpayers to plan effectively. Congress does this by delaying the passage of key tax provisions until the end of the tax year.

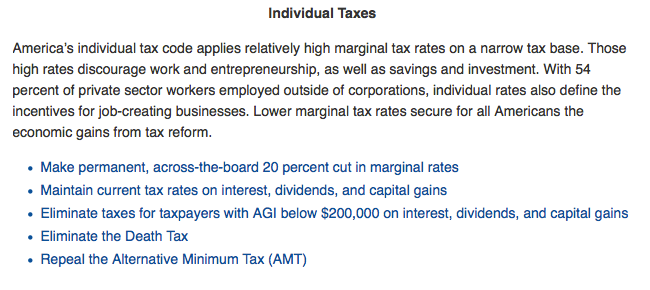

The debates are over and we are now less than two weeks from the election! There's a lot riding on this election for both nominees and both parties, but more importantly, for the American public as a whole. While there are numerous issues that will no doubt require the next President's attention, along with that of our lawmakers, few issues are likely to generate more interest from the American people than the subject of taxes.

Medicare will be a difficult challenge to the winner of this year's Presidential election. The number of Medicare recipients will be increasing as millions of baby boomers retire, and costs have increased as medical care has become much more expensive. Most experts agree that Medicare is unsustainable without raising taxes and/or reducing spending.

Recently, Presidential candidate Mitt Romney indicated that a $17,000 cap on itemized deductions could be used as a way to

help pay for his plan to cut tax rates across the board.This has caused some to wonder how their deduction for an IRA contribution would be affected by such a provision.Thankfully, the answer is both favorable and easy to understand. It wouldn't be! That's because IRA deductions are

not itemized deductions and therefore, would not be impacted at all.

{kind=link}